Who Owns the Future? (6 page)

Read Who Owns the Future? Online

Authors: Jaron Lanier

Tags: #Future Studies, #Social Science, #Computers, #General, #E-Commerce, #Internet, #Business & Economics

It was only recently that computation became inexpensive enough to be used to hide bad assets. The toxic financial concoctions of the Great Recession grew so complex that unraveling them could become like breaking a deep cryptographic code. They were pure creatures of big computation.

Even legitimate commerce can become a little scammy when some money remembers more than other money. There’s an old cliché that goes, “If you want to make money in gambling, own a casino.” The new version is “If you want to make money on a network, own the most meta server.” If you own the fastest computers with the most access to everyone’s information, you can just search for money and it will appear.

An opaque, elite server that remembers everything money used to forget, placed at the center of human affairs, begins to resemble certain ideas about God.

The Information Technology of Optimism

Economics is still a young field, often unable to definitively falsify theories or achieve consensus on basic tenets. Much of this book concerns wealth creation, for instance, and yet a consensus on where wealth comes from remains elusive.

1

I make no claim to be an economist. As a computer scientist, however, I consider how information systems evolve, and that can provide a window on economics that might be of use. Any information technology, from the most ancient money to the latest cloud computing, is based fundamentally on design judgments about what to remember and what to forget. Money is simply another information system. The essential questions about money, therefore, are what they always have been with information systems. What is remembered? What is forgotten?

When professional economics is unsettled, popular ideas about wealth creation can veer toward paranoia when it comes to wealth creation. Widespread wealth creation is hard to separate from “growth,” but growth is sometimes portrayed from the “Left” as a cancer that must eventually swallow both the environment and people. The “Right” is as likely to have an allergy to inflation, which happens at least a little when wealth expands broadly, along with an unbendable allegiance to austerity. It is remarkable that opponents hold such similar opinions.

Wealth creation, in the terms of information science, simply means aligning the abstract information we store with the concrete benefits we can potentially enjoy. Without that alignment, we will not enjoy all that we can.

For quite some time now, much of the new money brought into the world has actually been a memorialization of behavioral intent. It has been an account of the future as we plan it rather than the present as we measure it. Modern ideas about money answer the need to balance planning against freedom. If we made no promises of consistency to each other, life would become treacherous.

So we make promises to live by, but create degrees of freedom by choosing which promises to make, and how to keep them. Thus

a bank makes a loan based on confidence you can pay it back, but there is latitude in how you’ll do it, and multiple banks compete in part by having different heuristics to assess your loan-worthiness. What an interesting compromise we’ve come up with, allowing both freedom and planning!

This has been one of the key gifts of modern, future-oriented money. By making an abstract version of the essence of a promise (such as to repay a loan), we minimize the degree to which we have to otherwise conform to the expectations of one another. Just as money forgets the past, sparing us uncountable blood feuds, it also became a tool to abstract the future, allowing us to accept each other only to the minimum necessary degree needed to keep promises we’ve made.

This is what can happen when you buy a house with a mortgage in the context of the much-maligned fractional reserve system. Some of the money to pay for your house might not have ever existed had you not decided to buy. It is invented “out of thin air,” to use the language of critics of the system,

*

based on the fact that you have made a promise to earn it somehow in the future.

*

Both progressives like Thom Hartmann and libertarians like Ron Paul assail the fractional reserve banking system. It is often deemed “fraudulent,” a tool of “international bankers,” or a form of indentured servitude. While I agree there is a tremendous cause to criticize the present system, the venom seems directed at basic principles that deserve to be understood in a better light.

Ordinary people can help create new money by making promises. You constrain the future by making a plan, and a promise to keep to it. Money is created in response, because in making that promise you have created value. New money is created to represent that value.

This is why it is possible for banks to fall apart when people don’t pay their mortgages back. Banks sell assets that are partially made of the future intents of borrowers. When borrowers do something other than promised, those assets no longer exist.

An economy is like a cosmology. An expanding market, like an expanding universe, has unique laws and local phenomena. Growth is necessary in a healthy market, and it doesn’t have to come at the expense of the environment or other precious things we hold in common. Growth is merely honest if the goodwill of ordinary people is to be acknowledged instead of forgotten. That means a little

inflation—not too much—is proper, as people get better at doing things in ways that are acknowledged to be good for one another.

*

This is such a basic idea that it can be hard to see.

*

Yes, decrepit governments have been known to print money for its own sake, throwing a market into a death spiral. The creation of fake value is just as bad as the refusal to acknowledge real value.

To lose trust in the basic inception of wealth is to lose trust in the idea of human improvement. If all the value that can be already is, then market dynamics can only be about churn, conflict, and accumulation. Static or contracting economies make people cruel and shortsighted.

In an expanding market, new value and new wealth are created. Not all new wealth is created from game-changing events like inventions or natural resource discoveries.

†

Some of it comes from the ability of ordinary people to keep promises.

†

Historically growth also resulted from other factors like conquests and population growth, which are no longer sustainable.

The psychology of money hasn’t kept up with the utility of money. This is why the gold standard is so appealing in populist politics in the United States and keeps on recurring in libertarian circles.

‡

There is very little gold in the world, and its value is based on that scarcity. The amount of gold recovered from the earth thus far would fill only a little more than three Olympic swimming pools.

2

‡

The gold standard is admittedly something of a red herring (gold herring?), in that it isn’t a mainstream idea, though it remains commonplace in certain streams of American political thought. It is relevant, however, because the idea that there must be a hard limit to the amount of money in the world also drives most Silicon Valley–styled schemes to create new forms of money, like Bitcoin.

If the world were to run on a gold standard, then that stash would have to function as the memory of the global computer that humanity uses to plan its economic future. Therefore, the gold standard is a fundamentally pessimistic idea. Limiting our model of how to invent the future to the memory capacity of around 50 billion troy ounces

§

is just a way of saying the future holds nothing of surprising value.

§

The smartphone in my pocket as I’m writing this in 2011 has 32 gigs of memory, which is within an order of magnitude of the number of bits that are represented by all the ounces of gold in the world.

Money is only valuable as interpreted by people, so talking about the absolute value of money is meaningless, but we

can

talk about the information content of money. Counting what we might value in the future using only the bits already counted in the past undervalues what might be discovered or invented. It disbelieves in the potential of people to make promises to each other to achieve novel, great things. And the future has consistently proven to be grander than anyone dreamed.

The transformation of money into an abstract representation of the future (that thing we call “finance”) began about four hundred years ago and boomed in bursts ever since, as during the era of post–World War II prosperity. In order to understand what money had become by the time cheap digital networking appeared, remember that during the previous few centuries, wealth and well-being in industrializing societies expanded consistently in the big picture, despite periodic crashes and, of course, horrific wars. Even accounting for those many awful episodes, the future became impossible not to believe in.

Coincident with the European age of exploration and the echoes of the Enlightenment, an optimistic new kind of memory emerged, based on promises about future behavior, as opposed to what had already happened. Artificial memory became more person-centric out of necessity. There was no other way to define money regarding the future, or in other words, to engage in finance. Only people, not inanimate information, could make promises about what to do in the future. A dollar is a dollar whoever holds it, and securities can change hands. But a promise belongs to someone in particular or it is nothing.

The recent breakdowns of finance can be understood as the symptoms of a fallacious hope that information technology can make promises on its own, without people.

CHAPTER 4

The Ad Hoc Construction of Mass Dignity

Are Middle Classes Natural?

The advent of finance in the last four centuries or so coincided with rising ideals, the introduction of technologies that brought comfort and health to millions of people for the first time, and even the miraculous, imperfect rise of middle classes. In the context of this transformation, it is natural to ask why more people could not benefit from modernity sooner. If technology is getting so good, and there is so much wealth, why should there still be poor people at all?

Technological progress inevitably inspires demands for greater benefits than it has delivered at a given time. We expect modern medicine to be mishap-free and modern planes to be crash-proof. And yet, a century ago it would have been unimaginable to be even able to want these things. Modern finance similarly pairs benefits with frustrations.

If finance is imagined as a great fluid of capital flowing about the world, it will seem to storm and accelerate into great vortices, just like any large body of fluid. Some vortices swirl upward and some downward. It has often been true that the poor get poorer and the rich richer. Karl Marx spent a preponderance of his energies on observing this tendency, but it did not take a microscope to notice it.

Attempts to stem the flow and replace finance entirely with politics by means such as Marxist revolutions turned out to be vastly

crueler than even the worst dysfunctions of capital. So the conundrum of poverty in a world driven by finance remains a challenge.

Marx wanted something that most people, including me, don’t want: a committee to make sure everyone gets what’s best for them. Let’s reject the Marxist ideal and instead consider the question of whether markets can be counted on to create middle classes as a matter of course.

Marx argued that finance was an inherently hopeless technology, and that market systems will always degrade into the rut of plutocracy. A Keynesian economist would accept that “ruts” exist but would also add that falling into ruts can be staved off indefinitely with interventions. While there are theories to the contrary, it seems that middle classes have thus far relied on interventions in order to survive.

Great wealth is naturally persistent, generation to generation, as is deep poverty, but a middle-class status has not proven to be stable without a little help. All the examples of long-term stable middle classes we know of relied on Keynesian interventions as well as persistent mechanisms like social safety nets to moderate market outcomes.

However, it’s possible that digital networks will someday provide a better alternative to these mechanisms and interventions. To understand why, we need to think about human systems in fundamental terms.

Two Familiar Distributions

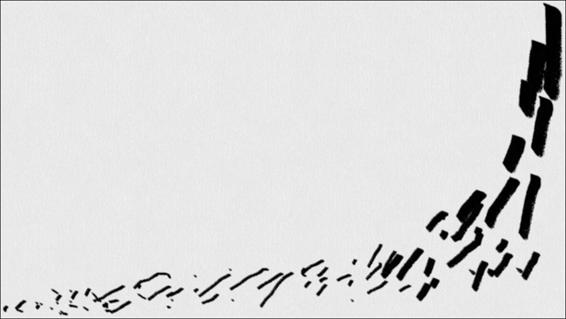

There are two familiar ways that people can be organized into spectrums.

One is the star system, or winner-take-all distribution. There can only be a few movie or sports stars, for example. So a peak comprised of a very small number of top winners juts out of a sunken slope, or a “long tail” of a lot of poorer performers. There are stars and wannabes, but not a lot of Mr. In-Betweens.