How to Create the Next Facebook: Seeing Your Startup Through, From Idea to IPO (3 page)

Read How to Create the Next Facebook: Seeing Your Startup Through, From Idea to IPO Online

Authors: Tom Taulli

Changing the world is not a part-time gig. It needs to be an obsession. When Jeff Bezos saw an opportunity to create an e-commerce company that sells books, he quit his high-paying job as a hedge fund manager, took his family across the country to Seattle, and along the way created the business plan for Amazon.com. Bezos (rightly) thought the Internet was a megatrend. Zuckerberg had a similar experience. He and several of his Harvard pals left school during the summer of 2004 and rented a house in Palo Alto to build Facebook. There was not much of a plan but he wanted to devote his full

attention to the website. By the end of the year, he decided to drop out of college.

These stories are fairly common. Consider Steve Streit, who lost his job in 1999 as a disc jockey. At the time, he had six kids and no job lined up. But he was passionate about his idea for a prepaid debit card. He put all his savings into creating a company, called Green Dot, to realize his dream. He eventually raised venture capital, struck a major distribution agreement with Walmart and took the company public in 2010 at a billion dollar valuation.

An entrepreneur needs to be highly committed and focused. Distractions can be fatal. True, there are some exceptions. Steve Jobs was able to run Apple and Pixar at the same time. But as we all know, people like Steve Jobs do not come around often.

As an up-and-coming entrepreneur, you need to care more about your mission than you do about anything else—including your company. Marc Bennioff, the founder of Salesforce.com, certainly does. I had a chance to talk to Bennioff during the early days when he founded his company, and I watched as its growth skyrocketed. For the most part, Salesforce.com created software for customer relationship management (CRM). CRM software is not very exciting to most people, but Bennioff found a unique way to deliver it to companies: He pioneered the cloud computing model, which meant that companies could access Bennioff’s CRM software via the Internet. This approach to distribution was disruptive, because traditionally software was installed on corporate networks and required lots of hardware and servers—not to mention high-paid consultants. Bennioff was convinced that the cloud would be much better. When I spoke with Bennioff, he rarely mentioned CRM. Instead, he railed against traditional software. To me, this was a much more interesting message than hearing about the features of a CRM suite.

As I got to know others at Salesforce.com, I quickly realized that they also deeply understood the company’s message about the power of cloud-computing and believed in it. There was never any confusion regarding this when I was talking to someone from Salesforce.com. Over time, Salesforce.com became the symbol of cloud computing. When businesses decided they wanted to adopt cloud-based solutions, the first place they turned was Salesforce.com. This brand advantage has allowed Salesforce.com to expand its platform to other software categories. As of 2012, Salesforce.com has a market value of more than $20 billion.

Many entrepreneurs want lifestyle businesses, which are not focused on strong growth. It is really about having an operation that provides enough profits to allow much more time for other interests. Who wouldn’t want to run a web site from, say, Maui, and spend a few hours a day working? Some people actually do this, and the endeavor can be lucrative, but these types of businesses do not generate much wealth. In this book, I look at those businesses that create wealth that is

life changing

. This means that there is often little time for anything but the business, so it helps to be passionate about the business in the first place.

Building a megabusiness may seem like a huge risk, but there are certainly some benefits from doing so. For example, large companies have a much easier time recruiting talent. Who doesn’t want to work for a company that has a big opportunity ahead of it? In addition, it is much easier to secure venture capital if you are seeking funding to create a large company. Few venture capitalists (VCs) even consider supporting a company that is gunning for a market opportunity less than $1 billion. For them, investing in smaller companies is just not worth the risk.

Despite this basic reality, I run into a lot of entrepreneurs who do not realize the importance of size and who try constantly to nab introductions to VCs to no avail. I do my best to steer them in the right direction and mention that they might need to rethink their goals—that is, to think on a grand scale. For the most part, thinking big is not easy for entrepreneurs, and as a result, their efforts to raise venture capital are often quixotic.

Now, thinking big does not mean you become a success automatically, but doing so will likely give you some downside protection. How? Let’s consider an example: Suppose you start a company that is focused on a market that has a $2 billion potential. After several years of hard work, you reach revenues of $50 million. Although your company is nowhere near to becoming the next Facebook, you have still achieved a great outcome and your company certainly has value! Now let’s say you decide to sell it. Even if you do not make a substantial amount from this deal, because your VCs will probably get the lion’s share from the sale, you are still considered “bankable.” You can take your lessons learned from this experience and then roll them over into your next venture. You probably have a few million bucks in the bank, as well, to start your next business.

This is the process that Mark Pincus, one of the original investors in Facebook, went through with several ho-hum startups. However, by 2007, he had

leveraged his experience and network to create Zynga. By late 2011, he had raised $1 billion in an IPO and was put on the Forbes Billionaires List.

Someone else who thinks big is Elon Musk, who has affected various industries and millions of people across the world. His entrepreneurial journey has been far from easy—and his ventures have endured several near-death experiences—but he has learned from every step along the way. Musk started coding when he was 10 years old. He sold his first program, a game about space, 2 years later for $500. Then, in the mid 1990s, Musk started an Internet content publisher, called

Zip2

, which he sold for $300 million. His next venture was X.com, which focused on online financial services. To bolster growth, he merged the company with rival Confinity, which was cofounded by Max Levchin and Peter Thiel (the latter was an original investor in Facebook). The new company became known as

PayPal

, but it had a high burn rate and nearly ran out of cash. Thiel managed to raise some much-needed capital in April 2000. The company went public and was sold for $1.5 billion to eBay in late 2002.

Although Musk could have retired easily after the sale of PayPal, he was still restless to change the world, so he invested much of his net worth in several megaconcepts. One was Tesla Motors, which develops electric cars. However, during the financial crisis of 2008, the company very nearly went bankrupt, endangering Musk’s finances in the process. Somehow, though, Musk was able to raise enough capital to save the company, and in June 2010, he took Tesla Motors public in the first IPO of a U.S. automaker since Ford went public in the mid 1950s.

Meanwhile, at the same time that Musk was building Tesla, he was also creating SpaceX, which develops space launch vehicles. He used innovative engineering techniques to accelerate the manufacturing process and snagged a $1.6 billion contract from the National Aeronautics and Space Administration. In May 2012, SpaceX launched and delivered cargo successfully to the international space station. The only others to do so include the governments of the United States, Russia, and China. Oh, and Musk is only 40 years old.

It’s a gruesome fact that most startups fail. They go absolutely nowhere. In light of this reality, it is amazing that entrepreneurs even start companies. Something must be wrong with them, right? Well, maybe entrepreneurs are wired differently. Although most people are risk averse, entrepreneurs

love

risk. They thrive on it. More important, to the most successful entrepreneurs, failure is not a stopping point. Instead, it represents yet another learning experience along the path to eventual success.

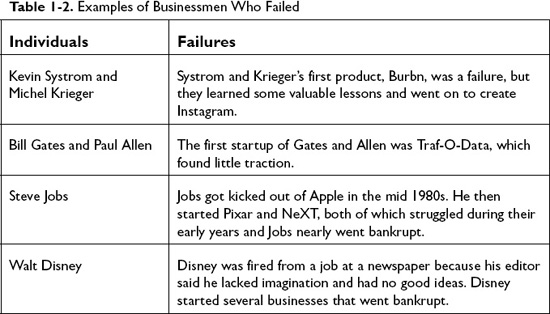

Even Zuckerberg has had his share of failures. Did you know that Facebook tried to launch a social network for the workplace? It was a disaster. So was Zuckerberg’s early mobile product, which used SMS (short message service) messaging to access Facebook. It was so complicated that people needed a chart to understand the functions. Then there was Beacon, which was a downright terrible idea. Beacon showed a user’s purchases to his or her friends, which created lots of problems; some people even found out about their birthday and Christmas presents! Beacon was so bad that it tarnished Facebook’s reputation, but Zuckerberg learned from these experiences and became stronger.

Success is a paradox: If you are not failing, then you are not succeeding. No one is perfect, including history’s standout business leaders like Steve Jobs and Bill Gates.

Table 1-2

presents a few examples of people who made mistakes but still came out on top.

When you experience a failure, keep that experience at the forefront of your mind. Try to learn helpful lessons from it. Failure isn’t fun, but the process can be extremely valuable, which reminds me of a true story. I won’t go into the names of the founders or the companies they created. Those details are not important. Rather, the lessons that were learned in the aftermath of the failure are what’s key.

Let’s rewind to the start of the Internet boom, in 1994. Two entrepreneurs, Jane and Joe, started their own Internet companies, both of which grew quickly. The market was certainly big enough for several strong players, and

the founders were able to raise several rounds of venture capital before taking their respective companies public. By the late 1990s, Jane and Joe were both worth billions. Then, suddenly, the Internet market gave way—and so did the valuations; Jane and Joe were now facing possible bankruptcy. To avoid the collapse of their companies, they raised money at low valuations and had to fire hundreds of people, many of whom were friends. It was an agonizing experience. However, what happened next was crucial. Joe saw the experience as a failure and became risk adverse. Even though his company was beginning to experience growth again, he moved his business along at a slow pace. He tried to avoid any long-term commitments, such as investing in new technologies or hiring people. Joe ultimately sold his company for about $700 million. True, this is a great deal, but it could have been much better.

You see, Jane did just the opposite. She continued to believe that her opportunity was huge, and she started to get aggressive with her investments. She hired more employees. She even struck several large acquisitions to add new products and customers. It was risky, but Jane’s company’s growth

exploded

. When Joe was selling his company for $700 million, Jane was selling hers for nearly $7 billion.

The content of blogs like Techcrunch, VentureBeat, and Pandodaily, and the stories about the entrepreneurs in this book may be intimidating to aspiring entrepreneurs. How can you compete? How can you raise the financing? Is your idea good enough? How do you build the right team? Before you get too overwhelmed, it is important to take some deep breaths and think about how other great entrepreneurs got their start. Steve Jobs and Steve Wozniak started Apple in a garage. Mark Zuckerberg started Facebook in a dorm. So, what is it that sets the Jobs, Wozniaks, and Zuckerbergs of the world apart? The answer is this: These founders started small, but they had lots of energy, passion, and focus. They also had little or no business or startup experience. Instead, they figured things out along the way.

So think big, but start small. As seen in the chapter, the “big” part is the mission, which should always be the driving force of the company. You should also be exceptionally passionate about it— almost becoming an obsession. Is your mission something you would quit your job for? If not, you probably should keep your job.

In the next chapter, we’ll get deeper into the process of building your venture. We’ll take a look at making sure you build a solid legal foundation.

A verbal contract isn’t worth the paper it’s written on.

—Samuel Goldwyn

Like many smart young software engineers, Mark Zuckerberg did a lot of contract work for an array of clients while he was in college. Often, these gigs were short term in nature, but they tended to generate thousands of dollars for him. In fact, the money actually helped him pay his way through Harvard.

However, Zuckerberg did not understand the risks of these engagements. What if he developed a product or program that ultimately conflicted with the creation of Facebook? Might he be giving away his valuable intellectual property? As it turned out, the contract work that Zuckerberg undertook as a college student turned out to be a real source of legal problems for him and his young company, and Zuckerberg ended up making some big-time legal mistakes that cost Facebook dearly before he got the help of a qualified attorney.

In this chapter, we take a look at the legal blunders Zuckerberg made during his company’s infancy, as well as several strategies he could have used to avoid the many infamous legal headaches that Facebook has suffered. As you’re reading, soak up the legal lessons of this chapter and learn from Zuckerberg and Facebook’s mistakes, because nothing can bring a young company to its knees faster than a lawsuit (or 12). Just look at Napster.

When starting a new venture, it’s tempting to scrimp on legal fees. Why should anyone get hundreds of dollars per hour for their services? Aren’t the majority of legal issues that startups face fairly straightforward?

Not really. The law is critically important in any business endeavor, and the legal details of even the most everyday business transactions can get extremely complicated. Despite this well-known reality, many entrepreneurs still try to go solo when it comes to their legal issues, and they rely on a free Google search rather than a paid legal professional. They also try to find sample contracts online and then attempt to tailor them to their business’s needs. Obviously, this inadvisable practice can cause a world of trouble for young startups, because these legal documents may have already been negotiated or may be aligned with the laws of a jurisdiction other than that in which they operate.

Some founders, acquiescing to the necessity of obtaining some form of legal advice for their company, use third-party legal services like LegalZoom. Although companies like LegalZoom provide tremendous services at cost-efficient prices, they are often incapable of meeting adequately the needs of a technical startup with specialized issues that include the need to protect intellectual property. In addition, the fact that online legal services are named as such is a bit misleading, because they do not provide actual legal services. More accurately, they are document preparation services—and very good ones, at that—but you should not rely on them to serve as your company’s legal counsel.

No doubt, your best solution is to hire a qualified attorney who specializes in technical startups to advise your company in the many legal challenges it will undoubtedly face. Startup attorneys not only understand the nuances and landmines that are part and parcel of building a new venture, but they also realize that startups have little capital to spare. As a result, technical startup attorneys are usually willing to take equity as payment for their legal fees during a startup’s early days. Facebook, for example, issued 1.29% in equity to its first law firm.

Aside from sparing you the need to fork over huge amounts of cash in your company’s infancy, paying your attorney in equity effectively aligns their interests with those of your company. In other words, your attorney wants to see her equity in your company expand, effectively leading her to provide you with better legal counsel, which is a win–win for all involved. Also, most likely, you won’t be your technical startup attorney’s first client, which means that she probably has lots of contacts in the technology startup industry and might even be willing to make key introductions to potential investors.

Prior to hiring an attorney, make sure you perform some due diligence on your candidate pool. First, get a list of each candidate’s clients—either from fellow entrepreneurs or services like Avvo—and call them. Doing so is a good way to get a better sense of the caliber of the attorneys. Here are some other suggestions:

- Make sure you negotiate the attorney’s fees, and never take the first offer that she makes. This type of negotiation is actually expected and even customary.

- Insist that a partner work on your account, not a junior associate. Although you’ll pay a higher rate for the counsel of a partner, the quality of the work will be much better.

- Put a cap on admissible attorney’s fees. Why give a lawyer an excuse to keep billing and billing?

- Remember that attorneys are naturally conservative and have a tendency to focus on all the ways in which you and your company could get into legal trouble. So, when your attorney gives you legal advice, make sure you ask questions such as “What are the chances of getting in trouble?” and “What would be the consequences?” If the potential fallout seems minor or worth the risk, then you should purse that course of action even if an attorney has some doubts about it. Business is about taking calculated risks.

Now let’s take a look at Zuckerberg’s experience with obtaining legal counsel. Although Zuckerberg’s contract programming work was certainly helpful to him and Facebook, because it enabled him to build his business savvy and learn his craft, one of his contract projects turned into a legal nightmare for the company. In November 2003, twin brothers Cameron and Tyler Winklevoss as well as Divya Narendra met with Zuckerberg to develop a web site called

HarvardConnection

, which would host a list of upcoming parties and provide discounts for nightclubs. The Winklevosses and Narendra agreed to let Zuckerberg in on the deal. There was no written contract between the four parties, but there were many e-mail and instant messages that indicated that they had arrived at some type of agreement—part of which was, in exchange for equity in the enterprise, Zuckerberg would create the web site for HarvardConnection.

Zuckerberg was immediately given access to HarvardConnection’s server. However, despite stating initially that the job would be an easy one to complete, he failed to make much appreciable headway on the project. He claimed that he was swamped with schoolwork, but assured the Winklevosses and Narendra that he was working steadily on the site. Meanwhile, without ever having created functional code for HarvardConnection, Zuckerberg registered the domain name thefacebook.com and launched his own social networking site, which later became the phenomenon we all know today as Facebook. Upon hearing of Zuckerberg’s web site, the Winklevosses and Narendra quickly filed a lawsuit, claiming that Zuckerberg stole their idea for

a social network (they eventually created a college site called ConnectU). The litigation was finally settled in early 2008 for an estimated $65 million.

This experience was a classic, expensive mess, and Zuckerberg could have avoided this legal headache by taking a few simple precautions. First of all, after agreeing to work with the Winklevosses and Narendra on their web site, he could have insisted on a written contract and asked an attorney to review it prior to signing it. When becoming a partner in a new venture, it is essential that you sign a document that outlines each partner’s rights and responsibilities. Prior contract work and former jobs are often sources of problems for entrepreneurs who start new ventures, so think hard about your legal exposure—and about what papers you should or should not sign. Here’s some advice:

- Nondisclosure Agreement (NDA): Under the terms of an NDA, you cannot disclose material information to third parties—in general, for a fixed period of time, say, a year or two. These contracts can be broad but are usually enforceable. If you have signed an NDA and then start a company that is similar to your employer’s or your client’s, then the NDA could be a problem. Even if there is not an NDA in effect, the employer or client may be able to claim misappropriation of trade secrets. As a general rule, then, be wary about using propriety information when creating your own venture. Doing so could result in a nasty lawsuit.

- Noncompete: Under the terms of a noncompete agreement, you cannot compete against your employer or client for a set period of time—often a couple years. The good news is that noncompete agreements are generally not enforceable in California, but this is not the case with many other states. It’s yet another reason to create a company in California. Keep in mind, though, that if you signed a noncompete agreement as part of an acquisition, you may be held accountable if you do not abide by its terms. After all, you likely received payment for your efforts.

- Work-for-Hire: Typically found as a clause in a contractor’s agreement, a work-for-hire forces you to relinquish your right to the intellectual property to any work or product that you create for a client. Work-for-hires could cause you huge problems if you go on to form your own business based on work you completed for somebody else. Thus, if you plan to do contract work, it is probably best to avoid doing so in an

area on which you plan to focus when you start your own venture. If you’re an employee at a company, you will probably be asked to sign an invention assignment. Like work-for-hires, invention assignments give full ownership to your employer to all the intellectual property you create on the job. Some companies may even extend the time period in which this type of agreement is in effect beyond your last day of employment, such as for 6 months to 1 year. California, however, has some wiggle room. For example, if you create an invention during off hours, do not use company resources to invent it, and it is not relevant to your company’s business, then the employer has no ownership rights to it. An invention agreement may require that you disclose your activities, though. - Nonsolicitation: This type of agreement states that you are not allowed to poach the customers or suppliers of your employer. Interestingly enough, California looks unfavorably on these types of arrangements. Leaving an employer to form a startup is typical in Silicon Valley. In other words, even if you sign and ignore a nonsolicitation agreement in California, your former employer may not subject you to any litigation. In some cases, entrepreneurs may even get an investment from their original employer or may put together a customer or partnership arrangement. However, you should still be cautious when signing this type of agreement.

- Stock Options: If you work for a high-tech company, then make sure you understand your rights regarding your stock options when you leave the company. A stock options agreement usually permits you 90 days to exercise your vested options, but the sooner you do this, the better.

When should you incorporate? There are no magical answers to this question, and it seems—at least when it comes to legal matters—that this is typically the case. Here are some common triggers to consider incorporation:

- Hiring employees or contractors

- Talking to potential customers

- Talking to potential investors

- Securing a cofounder or two

These four triggers are all serious steps in creating a company, and it is much easier to pursue these efforts under the guise of a corporation. If nothing else, being incorporated lends you more credibility when talking to potential employees and investors, because they’ll know you have a certain level of commitment to the venture.

Here are some benefits of being incorporated:

- A corporation is critical when hiring noncitizens or nonresidents, because obtaining a visa is easier for these individuals if the business for which they are working is incorporated. In addition, international talent has become vitally important for technical startups.

- A corporation makes it easier to issue stock options, which is critical for technical startups.

- A corporation provides liability protection and ensures that the investors and officers are not held personally responsible for any debts or claims made against the corporation. Keep in mind, though, that you are not protected if you fail to maintain the formalities of the corporation, such as conducting board meetings and publishing an annual report.

If you incorporate your company earlier in its life span, you may also be required to pay less taxes if and when it comes time to sell. How is this so? Consider that if you own stock for more than 1 year before selling it, any gains you accrue on the sale are subject to a maximum federal taxation rate of 15% (not including any taxes levied by your state). If you do not hold the stock for at least a year, then you pay taxes at the ordinary rates, the maximum of which is 35%. For example, suppose you incorporate your business on January 1, 2012, and then launch your product in November 2012. Then, in February 2013, you decide to sell your company for $2 million. In this situation, you would get taxed at 15% because your shares in the company are more than 12 months old. It’s true that it may cost several thousand dollars to incorporate, and there are always ongoing expenses and filings involved with incorporating. However, when it comes to your venture, incorporation is a smart move—a move that, in the end, could save you potentially millions of dollars.